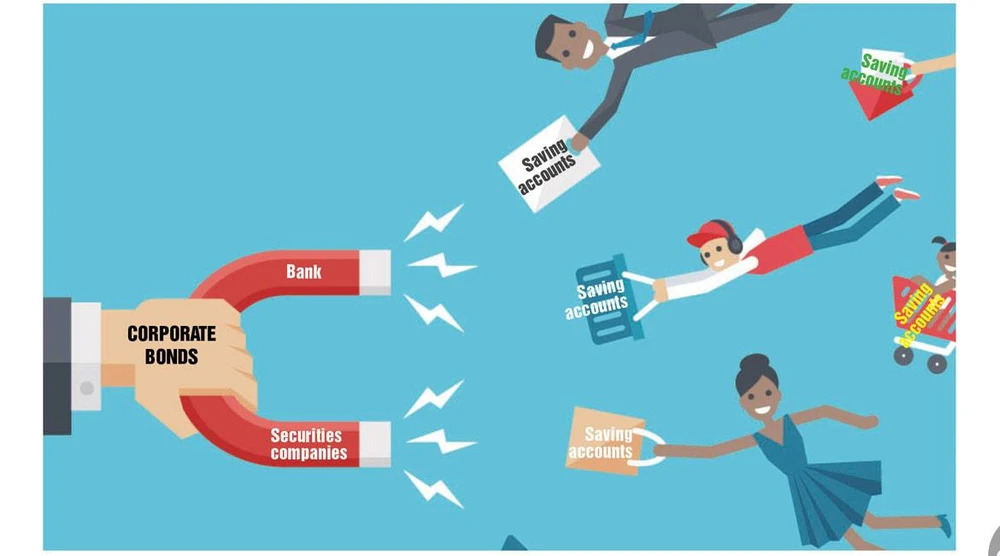

However, now the bond market has found ways to reach the pockets of even small savings depositors and lure them into using their dormant finances in an active money market.

Depositors lured

The author of this article has witnessed firsthand the luring of thrifty depositors into becoming corporate bond investors in the last two years. The author being a valued bank customer was invited to participate in an investment conversion opportunity talk at a bank branch. About a dozen small investors attended, and most of them were over 60 years old. The presented documents were full of diagrams and tables and few of these people could read them. The main concern of the participants at that time was how much the bond interest rates would affect their savings. They all were savings account holders who were on the bank radar with relatively stable balance sheets.

Two years ago, the author met with the General Director of a securities company in Hanoi, who was excited to reveal a strategic plan to develop investors accounts based on an interesting logic. He said that tens of millions of savings accounts that were lying dormant with huge sums of money could be turned into investment accounts if you knew how to convince the parties concerned. Therefore, a training program for brokers and account developers led to a number of new accounts opening at this securities company within only a few months.

Currently, nearly all major securities companies in the market are launching bond investment service packages to meet customer needs. VNDS has products such as D-Bond, V-Bond; MBS has Abond; SSI has Sbond; TCBS has iBond. Although the names defer, the common factor is that they help a customer to easily buy corporate bonds. On websites of securities companies, we can see a series of investment products offered in attractive wordings. There are even persuasive staff willing to go out of their way to assist potential investors.

Unruly bond market

If two years ago persuading savings depositors to buy corporate bonds was a major effort, now investment in municipal bonds has become almost a trend. Depositors are aggressively being lured towards bond investments with interest rates higher than in banks. Quality of customer service is of a high notch and potential investors are guided at every step, with all procedures well taken care of. The latest 4.0 technology also lends support.

With so much at stake, the corporate bond market has become unruly to some extent, with the addition of thrifty savings account holders along with real investors. Few corporate bonds are listed on the official stock market, and most bonds are traded on the OTC market. Even intermediary organizations such as banks and securities companies have created their own markets for their customers, making it difficult to quote effective prices. Whether the sale is reasonable in price or not depends mainly on the broker.

International corporate bonds only deal on the OTC market. However, in developed markets, the city is the domain of professional investment organizations, funds, banks or large investors wishing to diversify their portfolio. It is where traders and brokers compete with each other on behalf of customers, and experience and professionalism is considered a vital asset for judgement.

In the current corporate bond market in Vietnam, the majority of corporate bonds coming to savings depositors are bonds that have been issued separately. Very few professional investors join organizations involved in buying at the time of primary issuance. The intermediaries then cut a part of their profits and split up the bond lots to push them to the secondary market and to the savings depositors or other individual investors.

The daily purchase price is also at a discounted interest rate that very few people can calculate if it is reasonable or not. The only number to be emphasized is compared to the savings interest rate and even to the point where inflation is ignored.

Most of the savings account holders who have turned into bond investors cannot understand or evaluate the information from a broker because they do not have enough knowledge or experience. This unruly market lacks intermediary credit ratings for issuing businesses. It is strange that the issuer, even the company involved in re-issue, will sell the bonds to themselves.