Unexpected movement

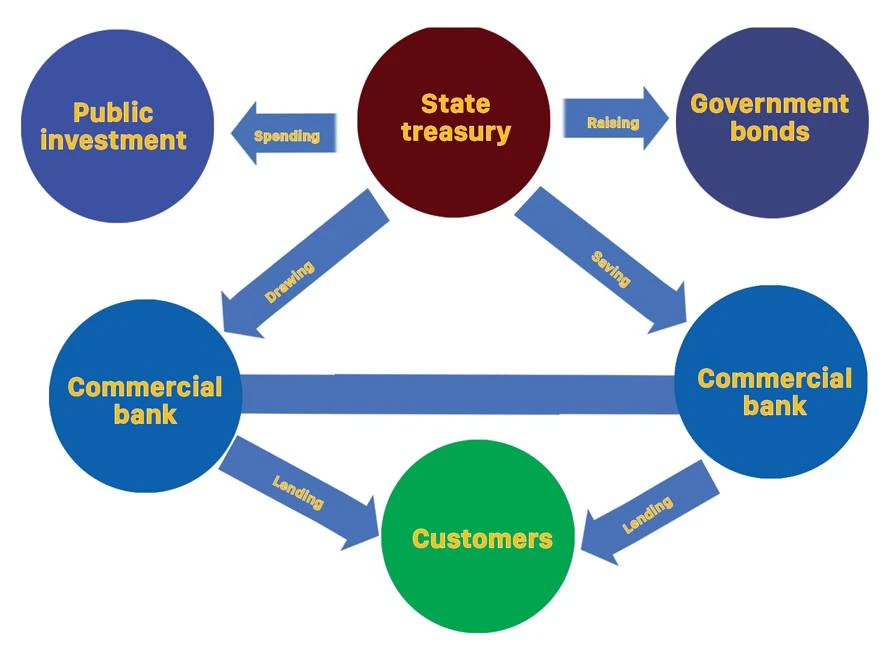

In Q2/2019, the State Treasury was successful in selling VND 35,600bn of government bonds. For the first six months of 2019, total proceedings from government bond issuance was VND 105,000bn, completing 70% of full year target of 2019. However, the speed of disbursement for public projects has been slower than expectations.

According to the General Statistics Office (GSO), the growth of public investment reached 2.1% in the first six months, in which the investment from the government issuance budget declined 14%, the investment from the national budget, which constituted the most in the total investment, rose 3.7%. Hence, a big amount of proceedings from government bond issuance has been put into the banking system and impacted the volatility of the interest rate in the market.

For example, at the beginning of the second quarter, while banks were under pressure from the increase of required reserve ratio of the State Bank, the State Treasury withdrew its money. These two factors have pushed up the interest rate on the interbank market. The overnight rate rose from 3.68% to 4.1%, and the rates of 1-week and 2-week terms also rose from 3.75% and 3.8% to 4.3%. The interbank interest rates in the interbank market have only fallen back since the end of April thanks to the deposit of the State Treasury.

A report of Sai Gon Securities Company said that the volatility of interest rate in the interbank market had been mainly driven by the movement of the cash flow of the State Treasury. At the end of April, the State Treasury had put a big amount of money into the banking system, causing the interbank interest rate to fall significantly. The interest rate in the interbank market only moves back to a normal level when banks successfully balance these funds.

The above example shows that the movement of the cash flow of the State Treasury has impacted the interest rate in the market significantly. Furthermore, the changing of the money amount put into the banking system by the State Treasury also impacted the market liquidity and this will be the challenge for the monetary policy in coming times.

Need consolidation between fiscal and monetary policy

There are some good impacts when the State Treasury opens an account at banks and put its money there. For example, when the State Treasury starts to invest in some projects, it just needs to do a money transfer to the contractors. It helps improve the management effectiveness and transparency of the public projects. However, most of the money amount that the State Treasury deposited at banks over the last three years was mainly for interest income earnings.

According to the Q2/2019 financial statements of Vietcombank, total deposit of the State Treasury at this bank at the end of June was VND 73,503, compared to VND 87,095bn at the end of 2018. The drop in deposit of the State Treasury mainly came from the drop in demand deposit of VND and foreign currencies. The term deposit of VND of the State Treasury at Vietcombank rose from VND 56,000bn to VND 67,000bn.

When public investment is implemented slowly, there will be a huge money amount of State Treasury in the banking system. This helps improve the liquidity in the market. However, the slowness of public investments creates pressure on the national budget as the government still has to pay the bond interest rate. Note that the money amount that the State Treasury deposits in banks is proceedings of government bond issuance.

There has been a challenge to consolidate the fiscal policy with the monetary policy. Since beginning of 2017, the State Bank of Vietnam has monitored the movement of cash flow of the State Treasury carefully. The State Bank has to decide whether it should issue the treasury bill to withdraw the money or buy back the valuable papers to pump money into the system. The State Bank of Vietnam sometimes even has to issue treasury bills with long-term maturity to reduce the liquidity in the system.

Since the beginning of the year to mid July 2019, the State Bank of Vietnam has withdrawn VND 105,506bn. Note that the interest rate of this money amount was not small. Furthermore, the huge deposit of the State Treasury at banks has kept the interest rate at a low level for a long time, narrowing the difference between VND interest rate and USD interest rate which consequently may create risk on the foreign exchange rate as banks may move to hold USD rather than VND.

Reversely, when the State Treasury withdraws its money, the State Bank has to pump money into the system. At the end of the second quarter, when the interest rate in the interbank market climbed to 4% as a result of low liquidity, the State Bank has to pump VND 47,000 into the market, in which VND 35,000bn via treasury bill purchasing and VND 12,000bn through OMO.

The National Assembly has just approved the Revised Public Investment Law to resolve the bottlenecks in public project implementation which is expected to push up the progress of all public projects. In Q3/2019, 3/11 routes of North-South Highway projects are planned to be constructed which will help improve the public investment disbursement. If this happens, the deposit of the State Treasury at banks will reduce and the State Bank will be under pressure to pump the money into the market to support the liquidity. Both these activities may create risk of inflation increasing. Note that the inflation rate has tended towards increasing recently because of several other factors.